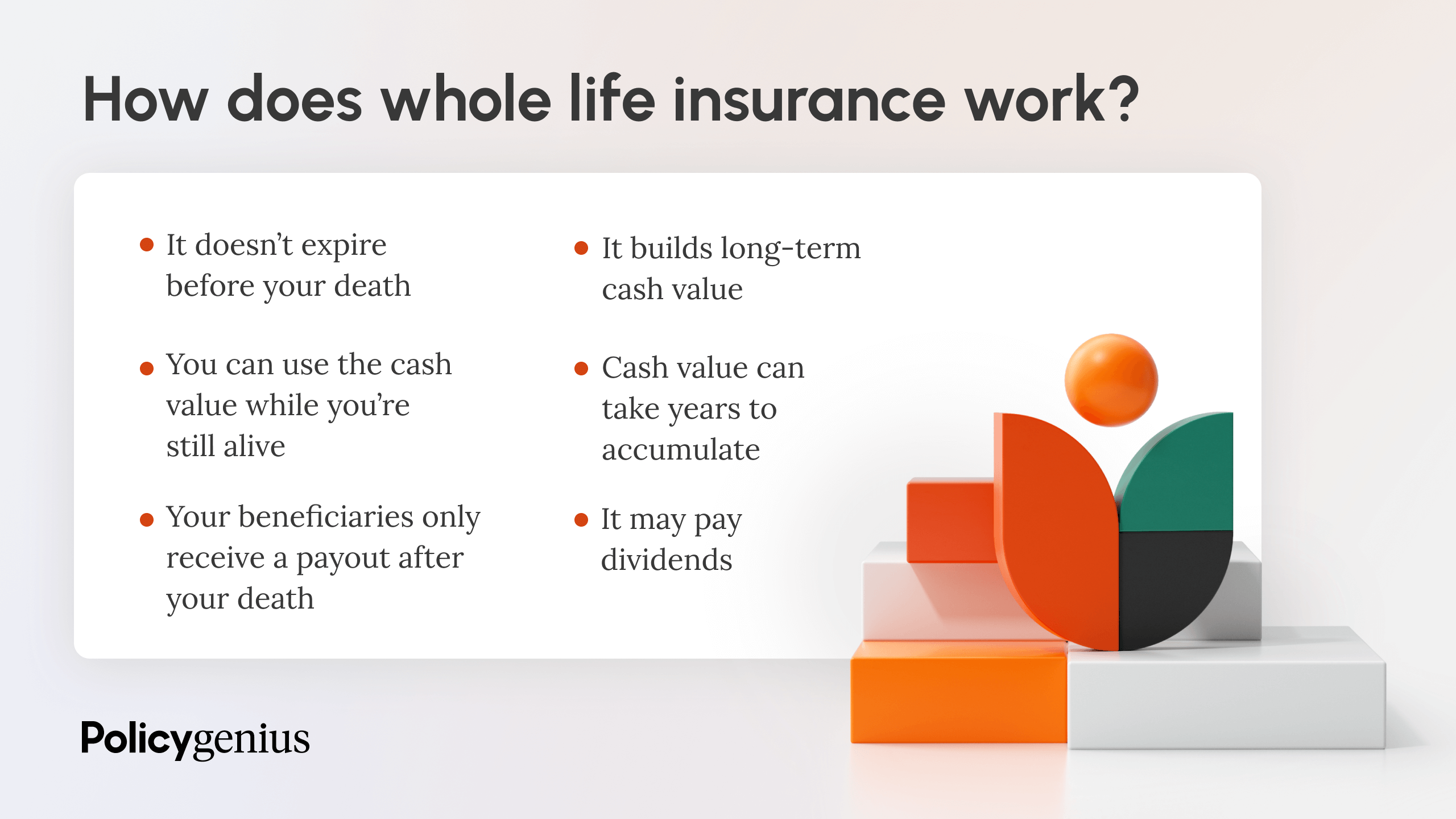

Is Life Insurance a Necessity or Just a Fear-Based Purchase?

The debate on whether life insurance is a necessity or merely a fear-based purchase often revolves around one's individual circumstances and financial goals. On one hand, proponents argue that it serves as a crucial safety net for families, ensuring that loved ones are financially protected in the event of an unforeseen tragedy. This perspective emphasizes the role of life insurance in providing peace of mind, allowing policyholders to look beyond their own lives and consider the potential burdens their absence may place on dependents. On the other hand, critics of life insurance often argue that it can be seen as a purchase driven by fear, where individuals may feel pressured to buy coverage out of anxiety over inevitable mortality rather than genuine necessity.

To determine if life insurance is a necessity, it's essential to evaluate your specific financial situation and responsibilities. For families with children, a mortgage, or significant debts, having a life insurance policy can be a prudent choice, providing funds that can cover these obligations and maintain a certain standard of living for the surviving family members. Conversely, for individuals without dependents, the discussion shifts; some may view life insurance as an undue expense, primarily motivated by fear of death rather than immediate financial need. In conclusion, whether life insurance is a necessity or a fear-based purchase largely depends on personal circumstances, financial responsibilities, and long-term planning goals.

Understanding the Real Benefits of Life Insurance: Are You Prepared?

Life insurance is often perceived as an unnecessary expense, yet it provides crucial financial security for your loved ones in the event of your untimely passing. The primary benefit of life insurance is its ability to offer a safety net. This policy can cover immediate expenses such as funeral costs, outstanding debts, and even daily living expenses, ensuring that your family does not face a financial burden during a challenging time. Additionally, life insurance can serve as a vital part of long-term financial planning, providing peace of mind that your dependents will be taken care of.

Moreover, life insurance policies can also accumulate cash value over time, which can serve as a source of funds for emergencies or major life events. If you're considering this financial tool, it's essential to assess your needs and understand the different types of policies available. In doing so, ask yourself: Are you prepared to protect your family's future? Evaluating your current financial situation and future goals can help you choose the right coverage level and policy type, ensuring that your family's financial stability is prioritized.

Life Insurance Myths Debunked: What You Need to Know

When it comes to life insurance, there are many common myths that can mislead customers and prevent them from making informed decisions. One prevalent myth is that life insurance is only necessary for those with dependents. In reality, life insurance can also benefit young, single individuals who may want to cover debts such as student loans or credit card balances. Additionally, securing a policy at a younger age can often result in lower premiums, which is a financial advantage.

Another misconception is that life insurance is too expensive for the average person. However, the truth is that there are various types of policies available to fit different budgets, including term life insurance, which is generally more affordable than whole life insurance. Furthermore, many insurers offer customizable options that allow you to tailor your coverage to suit your individual needs and financial situation. It's essential to assess your unique circumstances and explore the options available to you.